As expected, the memory crisis and rising smartphone prices have started showing their impact on global smartphone shipments. According to a recent Counterpoint Research report, global smartphone shipments in Q2 2026 have reached the lowest Q2 levels since 2013 as the memory crisis deepens.

It is revealed that DRAM and NAND prices continue to increase through the quarter as memory suppliers keep prioritising AI data centre demand over consumer electronics, forcing OEMs to pass rising Bill of Materials costs onto consumers by announcing price hikes, especially for entry and mid-tier smartphones.

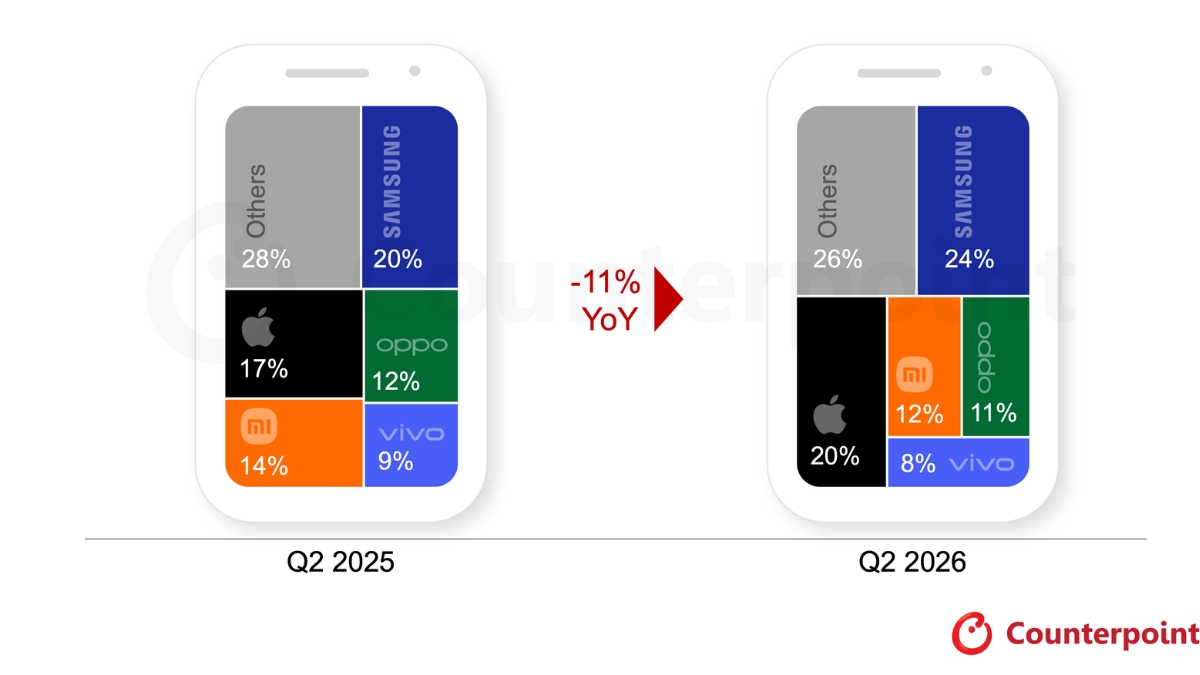

This resulted in global smartphone shipments falling 11% YoY in Q2, 2026, reaching the lowest second-quarter levels since 2013, according to preliminary estimates from Counterpoint Research’s Market Monitor.

According to Senior Analyst Shilpi Jain, “We see OEMs responded in different ways, some are increasing prices and accepting margin pressure, while others are extending the lifecycle of older-generation models and using promotions to retain budget-conscious buyers, and a few are simply pulling back on launches and production. Alongside the memory shortage, geopolitical tensions in the Middle East bumped up oil and shipping costs, further inflating smartphone prices. This coincided with a broader macro squeeze, slower global growth, higher inflation, and record-low consumer sentiment which hit price-sensitive buyers the hardest.”

Let’s take a look at the top 5 brands’ global sell-in shipment share (preliminary data)

- Samsung was at the top spot with a 24% share in Q2 2026. Samsung held up relatively well in India and the Middle East, supported by better product availability, fewer price hikes and aggressive summer promotions that complemented flagship momentum. Samsung’s Galaxy S26 series, vertical integration, expanded AI portfolio, and refreshed product lineup were factors in the overall growth.

- Apple was at the second spot with a 20% market share, while its shipments grew 3% YoY during the quarter. This is the only brand that avoided price hikes during the quarter. The iPhone 17 series remained the top-shipped global model, though China was a relatively soft spot as Apple’s shipments declined YoY, as this year’s discounts were less aggressive than the promotions.

- Xiaomi was in the third spot with 12% market share, while Oppo and Vivo ranked fourth and fifth in the market in Q2 2026, capturing an 11% and 8% shipment share, respectively. Despite being in the top 5 list, each brand recorded double-digit percentage YoY shipment declines in the quarter due to rising memory costs.

Apart from the top 5, brands like Google and Huawei have witnessed significant shipment growth in this quarter, rising 16% and 6% YoY, respectively. For Google, the growth was driven by Pixel 10 and 10a, while for Huawei, the Mate 80 series, Nova 15 and Enjoy 90 series played the key role.

Coming to the prediction for the rest of 2026, the report reveals that global smartphone shipments are expected to decline substantially, with the global memory shortage expected to persist next year as well. OEMs are likely to keep prioritising value over volume, while premiumization is expected to hold up relatively well through the remainder of the year. But overall demand recovery is unlikely until memory supply conditions improve substantially.