The first quarter of this year has not been quite fruitful for the Indian smartphone industry. According to IDC’s Worldwide Quarterly Mobile Phone Tracker, India’s smartphone market shipments declined 4.1% YoY to 31 million units in Q1 2026. Despite falling volume, the market grew 5.8% in value terms.

It is said that the Q1 2026 results hint towards a structural turning point for one of the world’s largest smartphone markets.

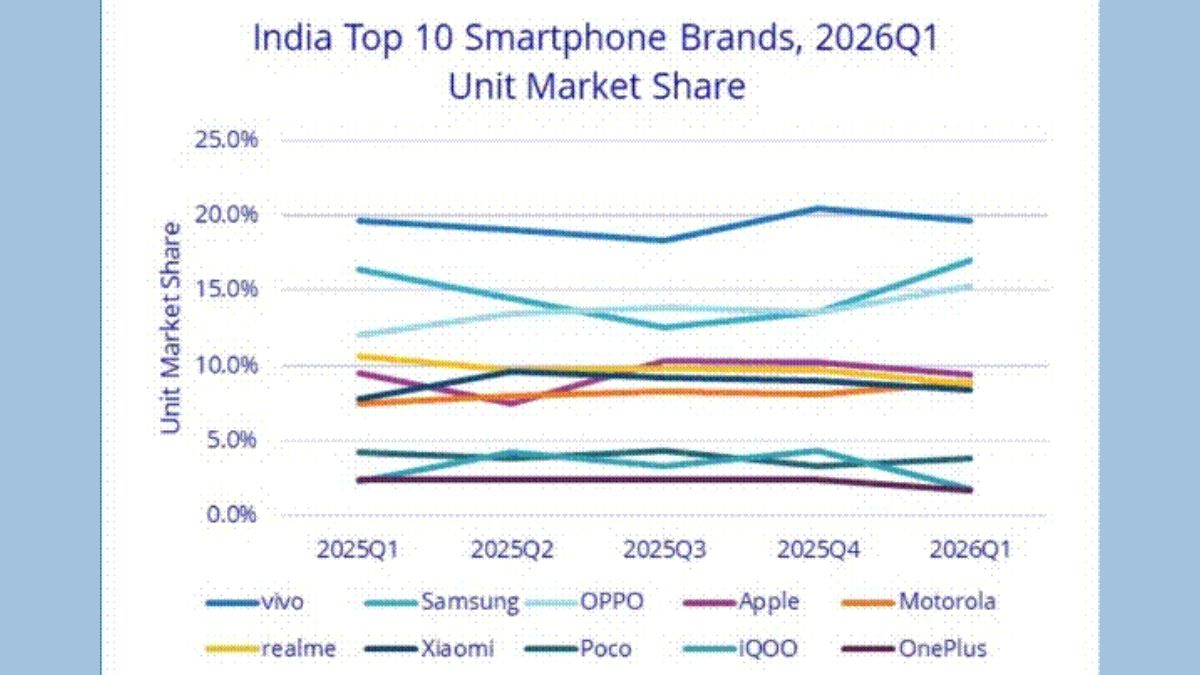

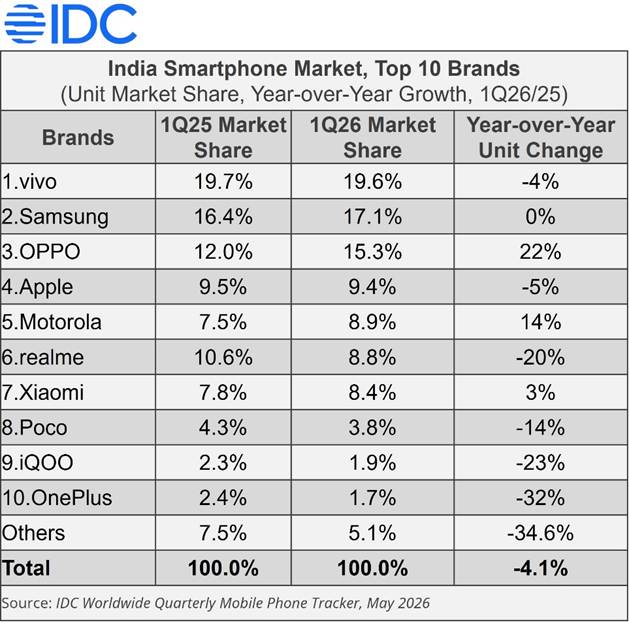

Top 10 brands in the Indian Smartphone market

As per the report, Vivo retained its top position with 19.6% market share, though it witnessed a decline of 4% in YoY unit change. Samsung was in the second spot with 17.1% market share, and Oppo secured the third spot with 15.3% market share. Apple and Motorola are in fourth and fifth spots, respectively.

Though Oppo is at the third spot, the brand recorded the highest YoY unit change (22%) among the other brands in the list.

The IDC report states that the decline in overall shipments was due to three converging forces: Memory cost inflation led to the fall of entry-level device shipments, the mass budget segment grew 10% YoY and rising input costs limited brands’ ability to deploy the aggressive discounting and channel-led promotions that historically fuel mass-market growth.

Price Band Performance

- Entry level (sub-US$100): 59% YoY; share fell from 18% to 8%

- Mass-budget (US$100-200): +10% YoY; share rose from 39% to 45%

- Entry-premium (US$200-400): -3% YoY; share edged up from 26% to 27%

- Mid-premium (US$400-500): +29% YoY; share rose from 6% to 8%

- Premium (US$600-800): +32% YoY; share rose from 4% to 6%

- Super-Premium (US$800+): -1% YoY; 7% share maintained

The offline channel share rose from 58% to 62%, while the online channel share came down from 42% to 38%.

“Average selling prices increased 10.4% YoY to a record US$302 in Q1 2026, driven by persistent memory cost inflation across both newly launched devices and existing models. Unlike previous quarters, aggressive discounting and channel-led promotional schemes remained limited, as rising input costs constrained brands’ ability to stimulate demand through pricing interventions. The current environment signals a broader structural shift in the market, where brands may increasingly need to rely on product differentiation, financing offers, and premiumization strategies rather than price-led promotions to drive demand through the remainder of 2026.” said Aditya Rampal, senior research analyst, Devices Research, IDC Asia Pacific.

It is said that the recovery in the second half will depend on how effectively brands balance product innovation, pricing strategy and cost management against sustained component inflation and uneven consumer demand.