India’s Wearables market declines 4.0% to 114 million units in 2025: Downturn primarily driven by a 17.6% YoY drop in smartwatch shipments

The International Data Corporation (IDC) recently revealed that, as per India’s Monthly Wearable Device Tracker, the Indian wearable device market fell 4.0% YoY in 2025, to 114.2 million units. As per the report, the primary reason for this downgrade was a 17.6% YoY drop in smartwatch shipments.

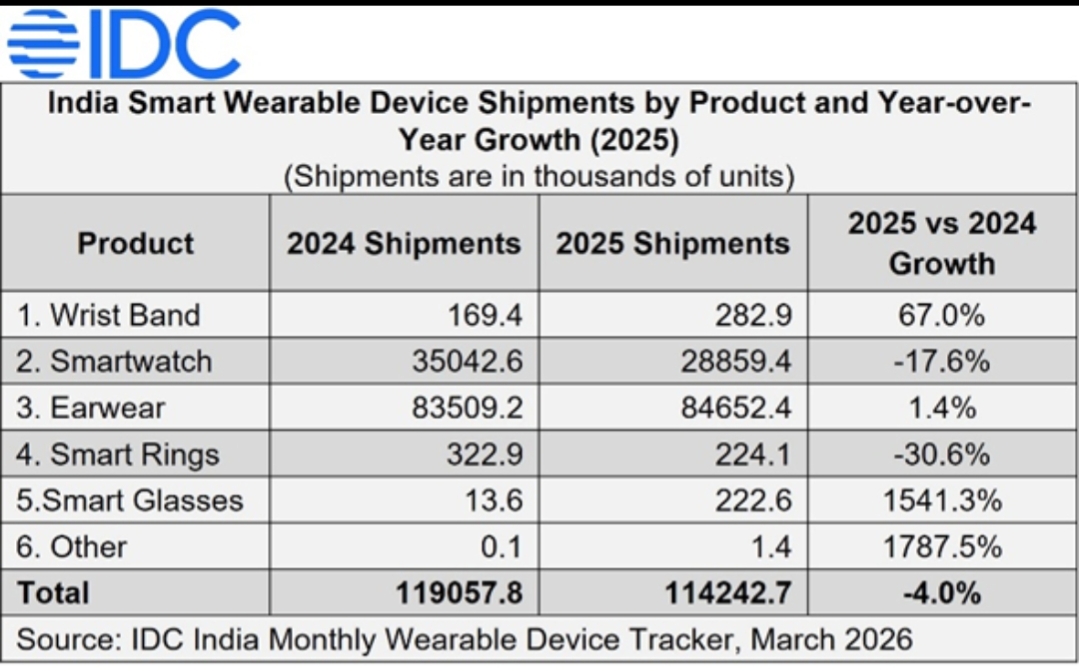

India Smart Wearable Device Shipments by Product and YoY Growth (2025)

The smartwatch shipment declined for the second consecutive year, falling 17.6% YoY to 28.9 million units in 2025. Despite lower volumes, the ASPs increased 11.7% YoY, rising from US$23.8 in 2024 to US$26.5 in 2025. Advanced smartwatch shipments declined 8.7% YoY in 2025, yet the market share rose slightly to 3.2% in 2025 (from 2.9% in 2024).

The wristband shipment saw a growth of 67% in 2025 (with 28.3 million shipments) when compared to 2024. The earwear category grew 1.4% YoY to 84.7 million units in 2025. The smart rings category saw a decline of 30.6%, while the highest growth in 2025 was witnessed by smart glasses- 1541.3%.

For smart glasses, Lenskart, Meta and Fire-Boltt led the segment, for smart wristbands- Samsung, Pebble, WHOOP and Amazfit led the segment, and for smart rings- Ultrahuman and Gabit led the category.

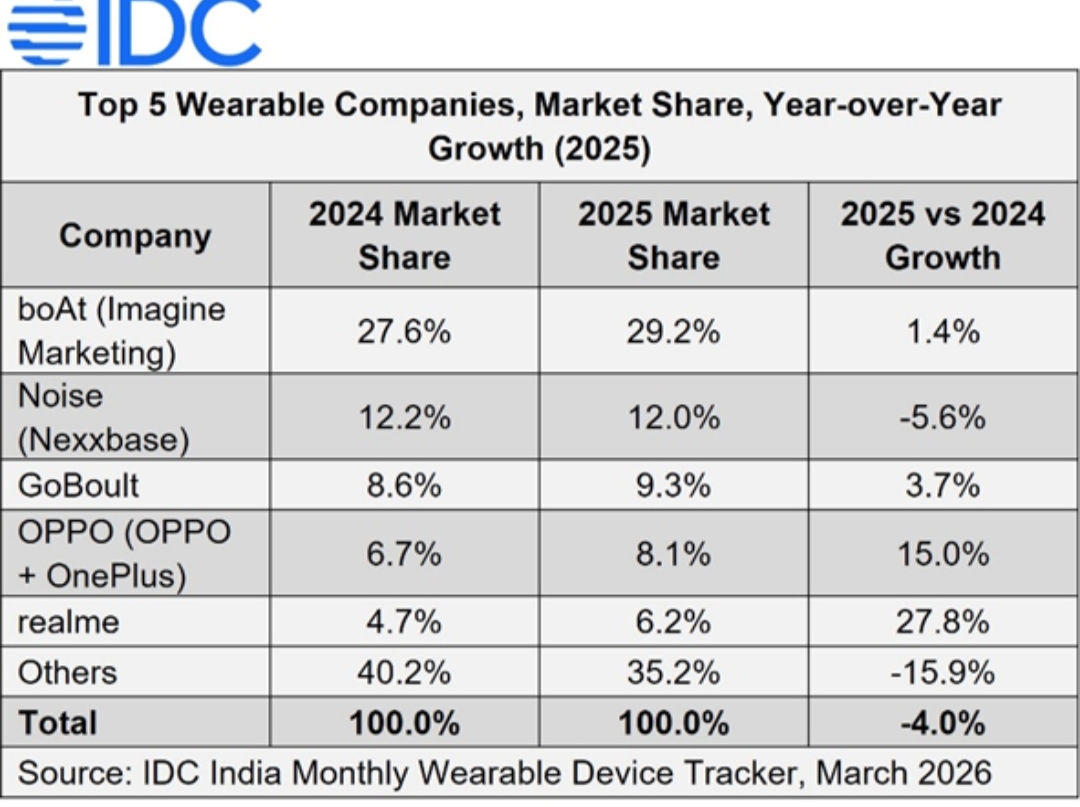

Top 5 companies in the wearable, smartwatch and TWS categories

Top 5 Wearable Companies

- boAt (Imagine Marketing)

- Noise (Nexxbase)

- GoBoult

- Oppo (Oppo+ OnePlus)

- Realme

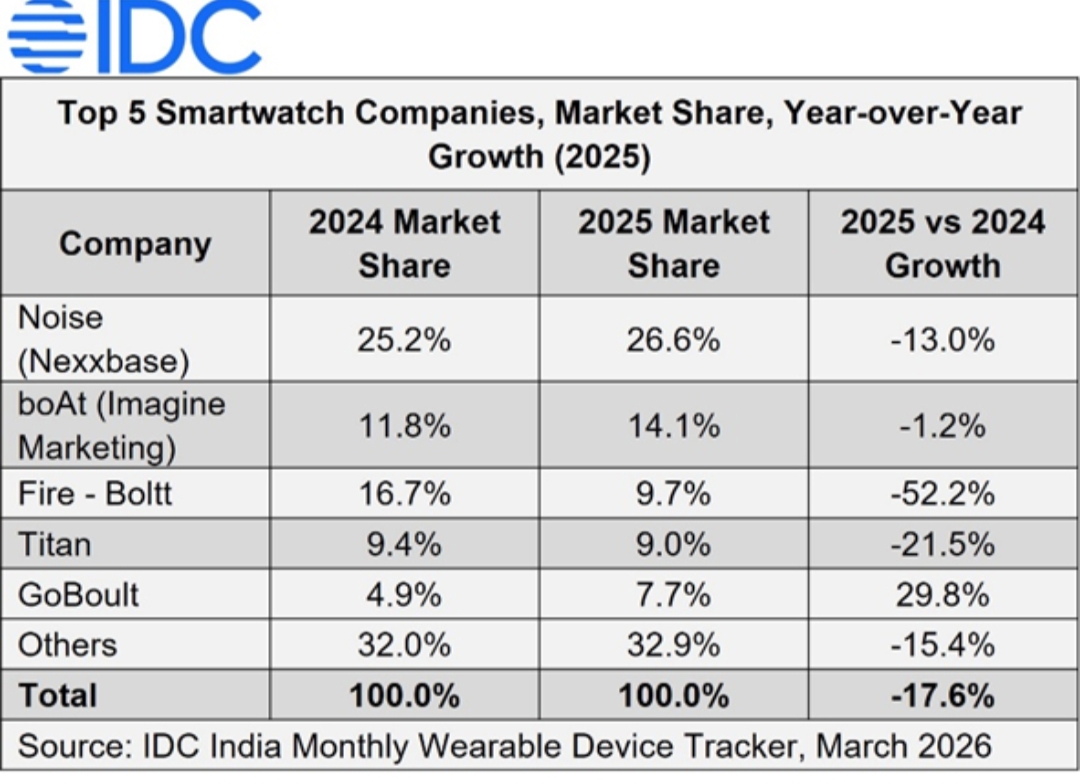

Top 5 smartwatch companies

- Noise (Nexxbase)

- boAt (Imagine Marketing)

- Fire-Boltt

- Titan

- Go Boult

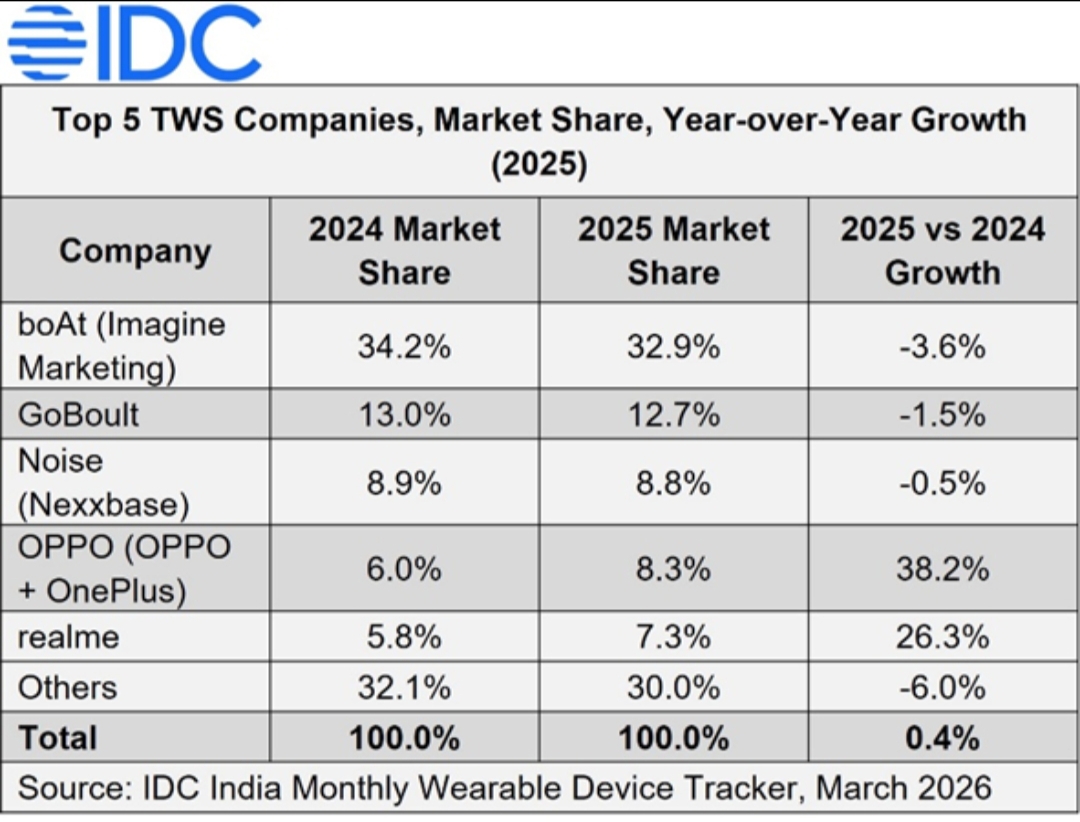

Top 5 TWS companies

- boAt (Imagine)

- Go Boult

- Noise (Nexxbase)

- Oppo (Oppo+ OnePlus)

- Realme

In the TWS segment, smartphone-led brands gained further traction in 2025; among them, Nothing (including CMF) recorded the highest YoY growth (91.5%).

In 2025, the offline channel strengthened further, growing 3.1% YoY and expanding its share from 37.8% to 40.7%, while the online channel declined 8.4% YoY. The online contraction was largely driven by a steep 22.7% YoY drop in smartwatch shipments, with earwear showing a relatively softer 3.2% decline. In contrast, offline earwear recorded 9.4% YoY growth, supported by stronger retail traction, although offline smartwatch shipments fell 10.5% YoY, highlighting a gradual shift toward offline retail channel penetration for stock push.